Private Loan Against Property in Ghaziabad Uttar Pradesh

We offer a private loan against property in Ghaziabad. Through our private lending, local companies or individual of Ghaziabad, who are facing difficulty in getting loans from regular banks, can avail private finance against their properties. This funding will be beneficial for: Some of the Key Features of our Private Loan Against Property in Ghaziabad

Private Funding Companies in India – An Alternative Finance Facility

India’s financial ecosystem has undergone a significant transformation in recent years. While banks and NBFCs continue to dominate the lending space, allowing only those with a good financial & credit profile to avail funds. Many companies or individuals skip some EMIs of an ongoing loan due to financial constraints, which can negatively impact their credit profile. Even some start-up companies having a vintage of only two to three years are also not eligible for funding from regular banks & NBFCs. So, there is an alternative financing for such credit issue companies or individuals through private funding companies. These private finance companies can lend money to such kind of low-CIBIL cases or companies having lesser financials compared to traditional banks. In this blog, we’ll explore what private funding companies are, how they operate, the types of loans they provide, and why they are becoming a preferred choice in India. What are Private Funding Companies? Private funding companies are the second line of financing option after traditional banks & NBFCs that offer finance to companies/individuals who have some credit or documentary issues. They are also called private lenders. Generally, they can finance the cases that are rejected by the conventional banks or NBFCs. Unlike banks, private lenders are Types of Private Funding in India Private funding companies or Private Lenders offer the following kinds of loans: Key Benefits of Private Funding Loans: Suitable for: Conclusion Private funding companies or private lenders can be a good alternative to traditional banks by offering faster approvals, flexible repayment terms, and solutions for high-risk or urgent funding needs. But on the other side of the coin, it is a much costlier option than a bank.

Loan Against Property Private Finance in Chennai

We offer loans against property from private finance in Chennai. Our services are useful when traditional banks refuse to provide funds due to some policies, such as low credit score or lack of documents. When financial needs arise, one of the quickest and most reliable ways to raise capital is by leveraging your existing property. A Loan Against Property (LAP) allows you to unlock the value of your residential, commercial, or industrial property while still retaining ownership. While banks offer LAP facilities, many borrowers in Chennai prefer private finance options due to their faster approvals, flexible terms, and simplified eligibility criteria. In this blog, we’ll guide you through the concept of Loan Against Property from Private Finance in Chennai, its benefits, eligibility, and how it can be the right solution for your funding requirements. What is Loan Against Property from private finance (LAP)? A Loan Against Property is a secured loan where borrowers pledge their property (residential, commercial, or land) as collateral to raise funds. The loan can be used for: Expanding or starting a business Managing working capital requirements Funding education or medical expenses Consolidating debts or settling loans Meeting personal or professional financial needs NPA Loan Takeover Unlike unsecured loans, LAP comes with lower interest rates and higher loan amounts because lenders have the property as security. Apply Now Why Choose Private Finance in Chennai? In Chennai, many businesses and individuals face challenges in availing loans from traditional banks due to: Low CIBIL Score / Poor Credit History NPA Accounts or Irregular Repayments Urgent Funding Needs Ongoing Legal or Compliance Issues This is where private finance lenders in Chennai come into play. They provide quick and customized LAP solutions with flexible repayment options. Key Advantages of Private Finance LAP: Faster Approvals – Loan disbursal within days, not months Higher Loan-to-Value (LTV) ratio compared to banks Minimal Documentation – Hassle-free paperwork process Flexible Repayment Tenure – Tailored as per borrower’s cash flow No Strict Credit Score Requirement – CIBIL score not a major barrier Features of Loan Against Property in Chennai (Private Finance) Feature Details Loan Amount ₹50 Lakhs – ₹50+ Crores (depending on property value& Type) Interest Rates Flexible, based on lender & risk profile Collateral Accepted Residential homes, commercial buildings, industrial property, land Processing Time 10– 25 working days Tenure 1 – 15 years (customized) Eligibility for Loan Against Property (Private Finance) Private lenders in Chennai typically offer LAP to: Business Owners / SMEs – Needing working capital or expansion funds Salaried Professionals – For personal or emergency requirements Builders & Developers – For project funding and loan settlements Property Owners – Looking to monetize idle assets Documents Required While requirements may vary, common documents include: Property ownership documents Identity & Address proof Latest bank statements Income proof (for individuals) / Company financials (for businesses) Existing loan details (if applicable) Why Chennai Borrowers Prefer Private Finance LAP Chennai’s growing real estate market and thriving business environment make Loan Against Property a preferred funding tool. Private financiers in Chennai cater to those who: Need urgent funds for business or personal use Want to avoid the lengthy process of banks Require higher funding than banks usually provide Need support in regularizing NPA loans through refinancing Conclusion If you are in Chennai and looking for quick, reliable, and customized funding, opting for a Loan Against Property from private finance companies can be the best choice. It not only provides liquidity but also ensures you retain ownership of your property. At Fund Source India, we specialise in arranging Private Finance Loans Against Property in Chennai, tailored to meet your financial needs with flexible terms and quick disbursal.

How to Get a Loan for Resort Construction in India?

India’s booming tourism and hospitality industry has created a wealth of opportunities for entrepreneurs, hoteliers, and real estate developers. With domestic travel rising steadily and international tourism returning post-COVID, resort construction has become a lucrative investment. However, building a resort is a capital-intensive project, and that’s where resort construction loans come in. This blog will guide you through everything you need to know about getting a loan for resort construction in India, including eligibility, funding options, benefits, and key considerations. 📌 What is a Resort Construction Loan? A resort construction loan is a type of project finance specifically designed to meet the funding requirements in the development and construction of resorts or luxury retreats. These loans are provided for: 🏝️ Why Invest in Resort Construction? India is home to diverse tourism hubs — from beaches in Goa and Kerala to hill stations in Himachal and Uttarakhand, and heritage cities like Jaipur and Varanasi. Resort construction in such high-footfall areas offers: 📝 Eligibility for Resort Construction Loans To qualify for a loan, the developer or promoter must meet the following criteria: 📄 Documents Required 📊 Loan Features Feature Details Loan Amount ₹1 Crore to ₹100 Crore+ Tenure 10 to 12 years (depending on project) Interest Rate 12% to p.a. Collateral Resort Land and Building Disbursement In phases, as per construction stages Repayment Can include a moratorium period 🌟 Key Benefits of Resort Construction Loans 📍 Ideal Locations for Resort Loans in India Financiers show strong interest in funding resort projects in: These locations are already popular among tourists and have high occupancy potential. ⚠️ Things to Remember

How to Get a Loan Against Property from Private Finance

When someone fails to get a loan from the traditional banks & NBFCs, a Loan Against Property (LAP) from private lenders is a smart way to raise funds quickly using your residential, commercial, or industrial property as collateral. Whether you’re a business owner in need of working capital, vendor payments, trying to meet a payment deadline, or an individual looking to fulfill urgent requirements, private finance offers faster and more flexible alternatives compared to traditional banks. 📌 What is a Loan Against Property from Private Finance? A Loan Against Property (LAP) from private finance is a secured loan issued against a property to raise funds, in cases where the borrower fails to raise a loan from the traditional banks & NBFCs. It is opposite to the banks and NBFCs that require strong credit scores, income proofs, and clean financials; private lenders focus more on the market value and title clarity of the property. These loans are offered by private financiers, NBFCs, HNIs, and private investment firms. 💡 When Should You Consider LAP from Private Lenders? Private LAP is suitable when: Apply Now -for Private LAP 🧾 Documents Required for Private LAP While private lenders have fewer documentation requirements than banks, the following documents are typically needed: 🏗️ Types of Properties Accepted Private financiers generally accept: The loan amount is usually 50% of the current market value of the property. ✅ Benefits of LAP from Private Finance 💰 Interest Rates & Tenure ROI: Private LAP interest rates range between 16% to 20% per annum, depending on risk, location, and property value. Loan Repayment Tenor Tenures typically range from 1 year to 5 years, with options for bullet or EMI-based repayment. Disbursal On successful approval, the loan is disbursed within seven to ten working days. ⚠️ Points to Remember 📍 Cities Where to Get a Private LAP in India? You can get a private loan against property in cities like: 🔚 Conclusion A Loan Against Property from Private Finance is a powerful tool to fulfill urgent financial requirements when conventional banks are not extending their loan facilities. It also ensures faster approval, less paperwork, and flexible loan terms. Call Now

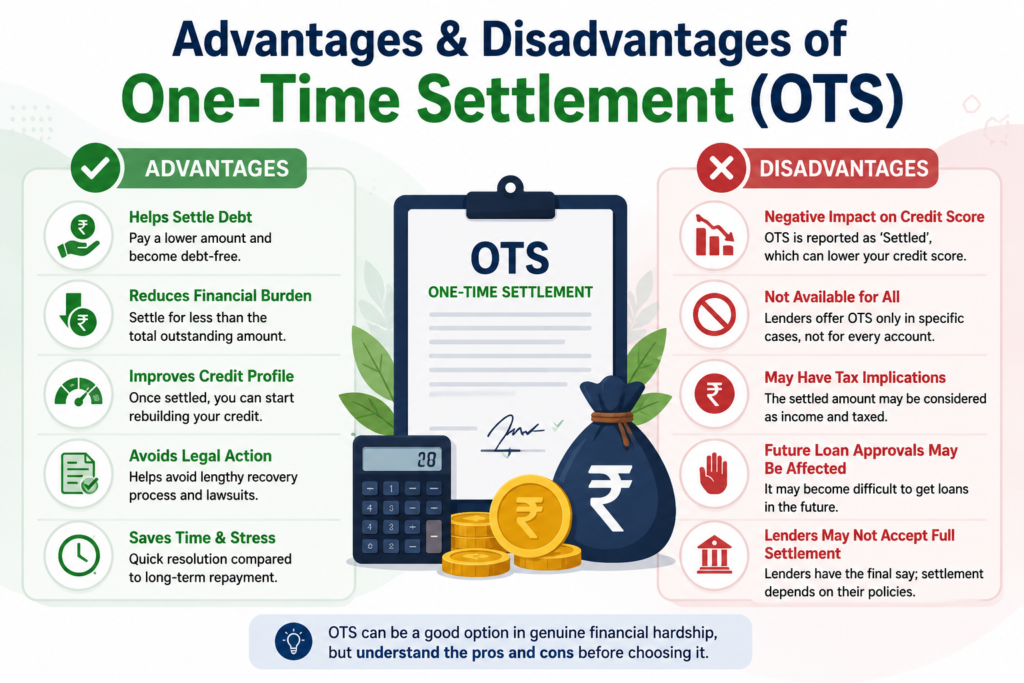

Advantages & Disadvantages of One-Time Settlement (OTS)

Every company or individual takes a loan in their life journey. Companies take loans for working capital requirements, for developing infrastructure & products like bank guarantees and LC to meet the business standards of clients. While individual takes loans to fulfill their requirement of child education & marriage, buying house properties, and renovation to buy their dream cars. Loans play a crucial role in a company’s growth and in fulfilling an individual’s requirements. So, their repayment is also crucial to maintain business growth and to avail loan facilities in the future. A good loan repayment ensures high credit availability with lower interest rates. On the other hand, a bad repayment not only creates legal issues for borrowers but also discourages other lenders from issuing new loans. So, in the case of non-repayment of any loan, companies & individuals have an option to close the account under the one-time settlement scheme, or OTS. Click Here – To get loan for your OTS What is One-Time Settlement or OTS in banking? One-Time Settlement or OTS is a scheme offered by banks to their NPA account borrowers who fail to pay their loans on time. Through OTS, the bank offers to close an NPA account at a reduced price, which encourages borrowers to get rid of their NPA liability in a single shot, whereas banks can collect a good part of the loan without long legal litigations. But is One-Time Settlement, or OTS, a good idea for a borrower to close the loan? Or what are the advantages & disadvantages of closing a loan under OTS? Advantages of One-Time Settlement (OTS) Disadvantages of One-Time Settlement (OTS)

What is Corporate Debt Restructuring?

Corporate debt restructuring (CDR) is the process of reorganising the outstanding loans of a financially stressed company to avoid defaults and maintain the company’s sustainability. In this process, certain loan terms are modified to offer a repayment plan that is convenient to pay while keeping the company stable: What is the main objective of CDR? The main objective of the CDR is to help companies regain their financial strength that are facing financial stress and are prone to default on their repayment commitment. This can be done by changing a few terms of existing loans, like increasing tenor, providing moratorium, and infusing additional working capital. Who Are Eligible Advantages of CDR to the Companies & Banks Companies have a number of advantages from the CDR: Advantages for Banks: Alternative Solutions to CDR The company can transfer its whole loan exposure/liability to a new financial institution. These institutions work as a bridge financier between the stressful situation to standard banking. This new financing offers the same benefits as normal CDR gives much better comforts, like: Fund Source India is a company known for offering such alternative solutions in difficult situations. Just apply through the form & their team will contact you. Conclusion Corporate Debt Restructuring (CDR) is a lifeline for businesses that are facing financial stress and on the verge of default. This helps them in coming out of the financial hardships and regain their strength. In return, CDR also helps banks to keep their books healthy and maintain their profits.

How to get finance for school?

Schools and educational institutions sometimes require financing or loans, whether for building infrastructure, upgrading facilities, or managing operational expenses. This is crucial for ensuring quality education and financial growth. With increasing demand for modern amenities and innovative teaching methodologies, schools and institutions often require financial support. To Get Funding For Your Hotel: Call Now The schools & educational institutions have multiple expenses and loans for such specific needs. The common requirements include: A clear understanding of the required amount and purpose will help identify suitable financing options. Five Ways Through Schools & Educational Institutions Get Finance 1. Bank Loans Banks offer different kinds of loans to schools and educational institutions to meet all types of funding requirements. These loans can be utilized for: Features: Drawback: Bank loans take a lot of time & paperwork for sanctions and disbursement. 2. NBFCs Loans (Non-Banking Financial Companies) NBFCs offer flexible funding solutions to schools & educational institutions and could be a better option than banks. Unlike traditional banks, NBFCs often have simpler application processes and quicker disbursements. Advantages: Drawback: NBFCs charge a little higher interest rates than banks. 3. Education Sector-Specific Funds Some government and private organizations offer grants or funds to schools & other educational institutions aimed at improving education. These funds often support: Examples: Government grants for schools under public-private partnerships. Drawback: Small funding sizes. 4. Promoter Funding Promoters can also fund the schools through their savings. Also, promoters can raise funds through secured & unsecured loans from banks & NBFCs, and loan funds can be utilized further to fund schools & educational institutions. Advantages: Drawback: A large amount cannot be raised through promoter funding. 5. Donations and Sponsorships High net-worth individuals and organizations may provide financial assistance to schools & educational institutions. Sponsorships can also be secured for specific projects, like setting up labs or conducting workshops. Choosing the Right Financing Partner When selecting a lender, consider: To Get Funding For School or Educational Institute: Apply Now Conclusion Schools and educational institutions can raise funds through various means, including traditional bank loans,s to more flexible and faster processes with NBFCs. And, the availability of grants & donations provides financial assistance for specific requirements. For expert assistance in obtaining finance for your educational institution, reach out to trusted financial advisors or lending partners who specialize in the education sector.

How Do Hotels Get Funding?

Starting or expanding a hotel business can be lucrative and profitable, but it often requires huge investments. Whether developing a new property, renovating an existing hotel, or requiring working capital, securing funding is one of the first and most critical steps. However, finding the right financing solution for your hotel project can be challenging — with various options, each suited to different needs and situations. To Get Funding For Your Hotel: Call Now Hotel funding can be utilized to fulfil the following requirements: In this blog, we’ll explore the various ways hotels can get funding, from traditional bank loans to more creative financing methods. Top Five Ways Through Hotels Get Funding 1. Traditional Bank Loans This is one of the most common ways to raise funding for hotels & resorts in India. The bank offers loans for the construction of a hotel to working capital requirements and loans to renovate an existing hotel. Banking finance suits the requirements of a hotel promoter like offering moratorium periods till the hotel becomes operational. Advantages: Disadvantages: 2. Non-Banking Financing (NBFC Funding) These days a lot of NBFCs offer loans for constructing or developing a hotel and resorts. NBFC processes loan applications faster than banks and requires less paperwork. These loans can be repayable in shorter to longer durations as per the borrower’s requirements. Also, the NBFC companies offer small to larger amounts of loans that are sufficient to meet the requirements of every borrower Advantages: Disadvantages: 3. Private Equity Funds and Venture Capital Private equity (PE) firms and venture capitalists (VCs) are another way to secure funding, particularly for larger hotel projects or innovative hospitality concepts. These investors typically provide funding in exchange for equity or partial ownership of the hotel. VCs can typically invest in start-ups or early-stage companies that have high growth potential. In exchange for their investment, these firms or individuals may ask for a share in the hotel’s ownership, decision-making power, and a portion of the profits. Advantages: Disadvantages: 4. Real Estate Development Funds If you are building a new hotel, some real estate funds can also offer loans for the construction of a hotel or resort. A construction loan provides the funds needed to complete the construction of the hotel. Real estate funds will be disbursed in the parts of each stage of construction (such as foundation work, framing, etc.). Once the hotel is completed, the construction loan can often be refinanced into a permanent mortgage or long-term loan. Advantages: Disadvantages: 5. Promoter Funding If the promoters are financially sound enough, they can fund the entire expenditure of hotel development. This type of funding is typically provided by the promoters in the form of equity or debt, and it plays a crucial role in the early stages of a company’s growth, especially when external financing options (like bank loans or venture capital) are limited or unavailable. Advantages: Disadvantages: To Get Funding For Your Hotel : Apply Now Conclusion Getting funds for hotels is not a tough task these days where a hotelier can get funds through multiple channels from traditional banks to private-equity financing and availability of real estate funds for the construction of the hotel.

NPA Funding by NBFC Companies

NPA Funding by NBFC Companies NBFC companies play a major role in providing loans in India. These companies offer funds for the specific needs of the borrowers. Generally, they offer loans at a relatively higher cost compared to banks, but they cover a larger profile that banks do not entertain. One of that profile are NPA accounts. These days, some new-age NBFCs offer funding for the NPA accounts as well as stress accounts. These companies have faster processes compared to banks, which makes them ideal for funding a distressed loan. They can fund an NPA account, SMA1, SMA2, and OTS transactions also. Borrowers Point of View Resolving the NPA account could be the priority for borrowers as banks take legal actions and try to sell off the borrowers’ precious property to recover their loans. All this put immense pressure on the borrowers to run their business as well as to save properties from banks. Borrowers are left with the options of selling their hard-earned properties or taking NPA funding from private lenders or NBFC’s. But again, private lenders charge high interest, which is not suitable for businesses already in stress. So, the better solution is to take funds from NBFC companies and close the NPA accounts. In the last few years, a lot of new-age NBFCs registered under the RBI that offer loans to close NPA accounts and are helpful in re-tracking the stressed businesses. So, the businesses that have good collateral coverage and a genuine repayment plan can avail funds from these companies and revive their business & save their collateral. Apply Now Benefits of NPA funding by NBFCs Companies: Direct takeover of the NPA account from the bank Loan for closing NPA account and OTS (One Time Settlement) Payment made directly into the NPA account Direct transfer of securities/collateral Freedom from NPA Status Update in CIBIL Score A new repayment track record Can avail of facilities from other financial institutions A moratorium period can be given Additional funds can be provided A new repayment tenor Standard mortgage of collateral properties Key Features of the loan offered by NBFC companies: A loan is offered to close the NPA account as well as for OTS Loans starting from Rs.1 Crore to any highest amount required Facility of pre-payment & part -repayments Option of a moratorium period up to six months Conclusion Availing NPA funding through the NBFC companies can offer multiple benefits to the borrower, like closure of stressed loans, saving their properties, revival of credit score, and offering working capital to run their business properly. Kindly download our Loan App